Need Help with AYB 339 Accountancy Capstone Integrated Case Study Assessment Answers? Get Case Study Answers on AYB 339 Accountancy Capstone Integrated Case Study. We Provide Financial Accounting Assignment Help, Accounting Case Study Assignment Help & AYB311 Financial Accounting Research Paper from Masters and PhD Expert at affordable price? Acquire HD Quality research work with 100% Plagiarism free content.

AYB 339 Accountancy Capstone Integrated Case Study

ASSESSMENT REQUIREMENTS FOR EACH PART

PART 1: Self-Reflection (10 Marks)

There is little doubt that COVID-19 has had a substantial impact on the way that this unit (and other units at QUT) have run this semester. For the first four weeks, students experienced how this unit is run in a face-to-face environment. However, from Week 4 onwards, discussion forums were moved to an online format.

This reflection asks students to self-reflect on the impact that COVID-19 has had on their studies in this unit, particularly given the large degree of groupwork involved.

Required:

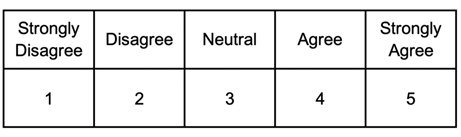

Using the 5-point Likert scale provided below, students are asked to rank their answers to each of following five questions on a scale from 1 to 5. Please write a brief explanation underneath each score as to why you awarded that particular score.

The five (5) questions are:

- I found the online discussions appropriately simulated face-to-face meetings and did not effect my communication with my peers and the facilitator.

- I now feel better prepared for working remotely and collaborating with clients and colleagues in the future.

- I would be comfortable and confident completing further education (CA, CPA, Masters etc.) in an online environment.

- Overall, I felt I was not disadvantaged by doing this unit this semester in an online format, rather in other semesters where the unit is run face-to-face.

- If I was offered a choice of face-to-face discussion forums or online discussion forums going forward, I would opt for face-to-face classes.

Your writing should be in the first person, that is, you should write your explanations with “In my opinion …”, or “I believe that …” This is very important as this assessment is a self-reflection so you must express your critical views and opinions on these issues.

You must use 11 point Arial font with 1.5 line spacing. Make sure each of your responses are clearly labelled. The maximum number of words is 1,000..

[Total for Part 1 = 10 marks]

PART 2: Enter Year-End Adjusting Journal Entries into MYOB & Print out a revised Profit and Loss Statement and Balance Sheet from MYOB – in pdf format (8 Marks)

A). Students are required to prepare and enter adjusting general journal entries directly into the MYOB data file to take into account all of the relevant and necessary adjustments (please include cents in all of your journal entries).

The MYOB data file is available on the AYB 339 Blackboard site for students to download. The MYOB data file was created using MYOB AccountRight Enterprise (Educational Version 19). This version of MYOB is available in the student labs in both B and Z blocks.

However, students can use any version of MYOB to open the data file and make adjustments (provided it is version 19 or higher).

It will not be possible to open this MYOB data file if you use the MYOB trial versions available on the MYOB website or any version of MYOB lower than this version.

The data file has been created in MYOB 19 for Windows. However, for those students who have an Apple Mac computer or laptop, the data file will be able to be converted and opened in Mac AccountEdge Pro. For those students who do not have MYOB loaded onto their Apple computer, we have provided the link to a compressed zip file containing the appropriate software to enable you to load Mac AccountEdge Pro v15.5 on your home or laptop computer.

These entries must be entered, produced and printed out using MYOB.

Make sure you use MYOB. Students cannot use other packages like Microsoft EXCEL or Word or any other accounting package.

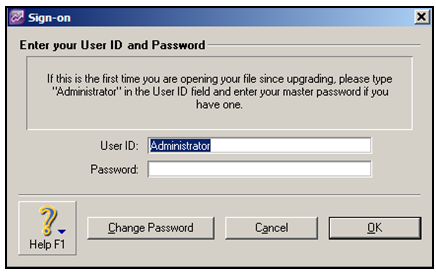

When you open up the MYOB data file, please use the “Administrator” User ID, as shown below.

B). Adding Account Names to the Chart of Accounts

Please note that students are expected to add additional accounts in the MYOB data file provided on the AYB 339 Blackboard site, as several of your adjusting general journal entries will be made to these new accounts (eg. depreciation expense).

C). Dating your Adjusting General Journal Entries 30 June 2019

Please date all of your adjusting general journal entries 30 June 2019.

Please also include a brief narration of the adjustment in the memo field in MYOB.

D). Printing Adjusting General Journal Entries at 30 June 2019 in pdf format

Make sure that you only print out your adjusting journal entries and not all of the other journal entries already residing in the MYOB data file that has been provided to you.

Simply select the General Journal function and the date range: 30 June 2019 to 30 June 2019.

E). Accounting Depreciation Entries

For accounting purposes, each individual depreciable asset listed on pages 19 and 20 of this case study should be depreciated over their useful lives based on the following straight-line rates (rate shown in the final column).

| Depreciable Asset | Accounting Useful Life | Depreciation Rate (Straight-Line %) |

| 1. Leasehold Improvements: § Fit-out (consisting of non-slip floor tiles, ducted air-conditioning, lighting, benches and signage) |

40 years |

2.5% pa. |

| 2. Property, Plant and Equipment: § Cash register § Desktop computer and printer § Refrigerators and freezers § Kitchen equipment and utensils § Ovens § Crockery, glasses and cutlery § Tables and chairs | 5 years 4 years 10 years 4 years 10 years 2 years 5 years | 20% pa. 25% pa, 10% pa. 25% pa. 10% pa. 50% pa. 20% pa. |

| 3. Computer Software: § MYOB AccountRight and retail point of sale software | 5 years | 20% pa. |

| 4. Liquor Licence: § Liquor licence | 2 years | 50% pa. |

| 5. Leased Motor Vehicle: § Leased motor vehicle | 8 years | 12.5% pa. |

There are a total of 11 individual assets (listed above).

However, instead of putting through 11 separate depreciation/amortisation journal entries, students are asked to only record five (5) journal entries in MYOB for each of the five classes of assets, namely:

- leasehold improvements (1 asset);

- property, plant and equipment (total of 7 assets);

- computer software (1 asset);

- liquor licence (1 asset); and

- leased motor vehicle (1 asset).

This means that you should enter five (5) depreciation/amortisation journal entries into MYOB.

For taxation purposes, being a small business entity (SBE), The Flavours of Italy Unit Trust will depreciate those eligible depreciating assets under Division 328 using the simplified depreciation regime (refer rules on page 29 of this case study).

F). Print out a Revised Profit and Loss Statement and Balance Sheet from MYOB as at 30 June 2019

Finally, students are required to print out a revised Profit and Loss Statement and Balance Sheet from MYOB for The Flavours of Italy Unit Trust for the year ended 30 June 2019 taking into account their adjusting general journal entries and include it in their submission.

In MYOB, your print range for the Profit and Loss Statement should be 1 July 2018 to 30 June 2019.

For the Balance Sheet, please print this report out as at 30 June 2019.

Please include cents when printing out both reports.

[Total for Part 2 = 8 marks]

PART 3: Prepare the 2019 Annual Report for The Flavours of Italy Unit Trust in Microsoft Word – (15 marks)

- Students must use Microsoft Word to prepare the annual report. Students are not permitted to use any other electronic account preparation software packages (eg. Handisoft, Xero, Solution 6, MYOB Accountants Office etc).

- When preparing the external financial statements, please round all figures from your MYOB management accounts to the nearest whole dollar. In other words, please do not include cents when preparing the external financial statements.

A). Students are required to prepare the Annual Report for The Flavours of Italy Unit Trust for the year ended 30 June 2019. The annual report should include the following documents (in the following order):

- the external financial statements excluding the Statement of Cash Flows, but including all of the notes to the accounts;

- the Trustee’s Declaration;

- Minutes of Meeting of the Trustee showing the accounting distribution of 50% to each unitholder; and

- the Accountant’s Compilation Report.

There is no need to prepare the financial statements for the corporate trustee, Flavours of Italy Pty Ltd, as the corporate trustee did not trade during the 2019 financial year.

For the Accountant’s Compilation Report, please use the name of the firm that you created and used throughout the semester for your PBLs.

B). Which Accounting Standards Apply?

For the purposes of this assignment, despite The Flavours of Italy Unit Trust being a small unit trust, please treat the trust as a reporting entity. In other words, please prepare general purpose financial statements for The Flavours of Italy Unit Trust.

In other words, please ensure that the 2019 financial statements (and notes to the accounts) are prepared in accordance with the recognition, measurement and disclosure requirements of all of the AASB Accounting Standards.

However, please do not apply the following five (5) AASB Accounting Standards:

- AASB 8 Operating Segments;

- AASB 107 Statement of Cash Flows;

- AASB 112 Income Taxes; **

- AASB 124 Related Party Disclosures; and

- AASB 133 Earnings Per Share.

** As the trust is not a separate legal entity for accounting and taxation purposes, no income tax accrues in the name of the trust. Hence, a trust does not have income tax expense (current or deferred). For this reason, AASB 112 has no application.

All other AASB Accounting Standards (including their recognition, measurement and disclosure requirements) must be complied with. This includes the suite of financial instruments standards (including AASB 7, AASB 9 and AASB 139, where applicable).

Please note that in the case of publicly traded financial instruments, The Flavours of Italy Unit Trust has made an irrevocable election under AASB 9 Financial Instruments to present subsequent changes in the fair value of equity instruments through Other Comprehensive Income (OCI) instead of recording increases and decreases in fair value through profit or loss.

Furthermore, the trust has elected not to early adopt any new Accounting Standards (eg. AASB 16 Leases).

There is no need in Note 1 Statement of Significant Accounting Policies to outline or consider the likely impact of the application of new AASB Accounting Standards that will apply in the future (such as AASB 16).

Finally, even though the trust is a reporting entity, it does not wish to apply the reduced disclosure requirements (RDR) contained in AASB 1053 Application of Tiers of Australian Accounting Standards.

C). Income Statement

For the Income Statement, Mario has requested that you classify expenses by function instead of by nature.

Mario wants you to show those expenses on the face of the Income Statement that are specifically required to be disclosed on the face under AASB 101 Presentation of Financial Statements.

Furthermore, please group relevant individual expenses in the MYOB profit and loss statement on the face of the income statement under the following headings: “employee benefits”, “depreciation and amortisation”, “finance costs”, “administrative expenses” and “other expenses”.

D). Statement of Comprehensive Income

When preparing the external financial statements for The Flavours of Italy Unit Trust, please ensure that you prepare and include a separate Statement of Comprehensive Income in accordance with AASB 101 Presentation of Financial Statements.

The trust wishes to adopt a two-statement approach in presenting their statement of profit or loss and other comprehensive income. In other words, Mario wants you to prepare an Income Statement and the Statement of Comprehensive Income separately.

F). Balance Sheet

For the Balance Sheet, please use the minimum disclosure requirements required under AASB 101.

G). “Real” and “Model” Financial Statements

Students are advised (and encouraged) to download the 2019 financial report of a unit trust and review the content, structure and format of the financial report.

Most unit trusts prepare general purpose financial report, so this will give students an excellent idea as to the layout, format, structure and content of a general purpose financial report.

Furthermore, some accounting firms, like PWC, have published model financial statements for unit trusts on their websites that students should consider referring to.

For example, a generic Google search on the term “model trust financial statements Australia” will list hyperlinks to several accounting firms websites where these model financial statements can be downloaded free-of-charge in pdf format.

I have uploaded PWC’s example (or model) financial statements of a unit trust on the AYB 339 Blackboard site.

Furthermore, a reminder that in the case of The Flavours of Italy Unit Trust, we are asking that general purpose financial statements be prepared for a trust, and not a company.

Furthermore, when preparing the external financial statements for The Flavours of Italy Unit Trust, please do not include the references to AASB paragraphs in the left-hand margin of the financial statements (or notes to the accounts) like the model sets of accounts do.

Finally, unit trusts (such as The Flavours of Italy Unit Trust) are not taxed. As such, no tax accrues in the name of the trust. Instead, the profits are distributed to the unitholders who include their individual distribution in the unitholders disclosed taxable income and pay tax on this in their name.

H). The Trustee’s Declaration and Comparative Figures

The Trustee’s Declaration should be dated 12 September 2019.

Comparative figures are not required in the financial statements, as the business only commenced trading on 1 August 2018.

The Minutes of Meeting of the Trustee showing the distribution of the accounting net profit (being 50% to each unitholder) should be dated 30 June 2019. There is no cash distribution of the accounting profit, but rather a notional distribution to each unitholder.

[Total for Part 3 = 15 marks]

PART 4: Prepare the 2019 Trust Income Tax Return and Tax Reconciliation for The Flavours of Italy Unit Trust – (7 marks)

A). Students are required to prepare the trust’s Income Tax Return & Tax Reconciliation for The Flavours of Italy Unit Trust for the year ended 30 June 2019

Students are required to prepare the 2019 trust income tax return of The Flavours of Italy Unit Trust. A blank copy of the 2019 trust tax return can be downloaded directly from the ATO website in pdf format at:

https://www.ato.gov.au/uploadedFiles/Content/IND/downloads/Trust-tax-return-2019.pdf

A blank copy of the trust tax return has also been placed on the AYB 339 Blackboard site.

The trust’s tax file number (TFN) is: 767 912 607. The business and postal address of The Flavours of Italy Unit Trust is:

144 Lancaster Avenue Phone: (07) 3161 7172

Hendra, QLD, 4011. Facsimile: (07) 3161 7174

Do not complete the BSB and account details on the second page of the tax return.

For the purposes of the tax agent declaration (on the last page of the tax return), your tax agent reference number is: 57134-006. Please put your name and contact details in this box.

The income tax return should be dated 12 September 2019. It should be signed by Mario.

In terms of the trust distribution of the net income to each of the two unitholders (ie. Item 55 Statement of Distribution), please use the personal addresses for both Mario and Luciano contained on page 21 of the business plan. The addresses can be used instead of providing the two tax file numbers of each family trust.

Students should also prepare the trust distribution minute (showing the 50% distribution of the net income of the trust estate – or tax profit – to each unitholder) for Mario and Luciano to sign. Please date your trust distribution minute 30 June 2019.

Like the accounting distribution, there is no cash distribution of the tax profit, but rather a notional distribution to each unitholder. This tax distribution Minute should be included immediately after the last page of the tax return.

There is no need to prepare the income tax return for the corporate trustee, Flavours of Italy Pty Ltd as the corporate trustee did not trade during the 2019 financial year and derived no income whatsoever in its own name.

[3 marks]

B). Students are required to prepare a One-Page Tax Reconciliation for The Flavours of Italy Unit Trust for the year ended 30 June 2019

Mario and Luciano also ask you to prepare a one-page tax reconciliation.

Students should start this reconciliation summary with the accounting net profit before income tax and then list all relevant adjustments to arrive at the trust’s net income of the trust estate (also referred to as the tax profit of the trust) for the year ended 30 June 2019.

This one page reconciliation should be included immediately behind the last page of the trust’s tax return. There is no need to prepare a deferred tax worksheet for this requirement.

Furthermore, when presenting your tax reconciliation, there is no need to refer or quote sections of the ITAA (1936), ITAA (1997), cases or taxation rulings.

Finally, please round all figures in the tax reconciliation to the nearest whole dollar. [4 marks]

[Total for Part 4 = 7 marks]

PART 5: Professional Approach to Presentation

This assessment expects a professional approach to presentation similar to that expected in an Accounting firm when delivering documents to a client.

For this reason, you must satisfy the following professional presentation requirements or you may incur penalties.

- A professional approach also means that it is the responsibility of each student to ensure that the complete assignment is submitted by the due date and in the correct format (see below).

- Once submitted, students are not able to attach or submit any additional documentation whatsoever as in a client situation, you would be unable to deliver additional information to a client and late information will be regarded as being late and may not be useful.

- As students will be submitting all parts of the case study via QUT’s Turnitin, students are asked to collate all of the various documents and save them into one pdf document to upload into Turnitin.

- Please name your file “Your Student Name – Integrated Case Study.pdf”.

- Please save the documents in pdf format in the order listed on page 16 of this case study.

- Students are also required to submit the signed student integrity declaration (contained on page 30 of this case study).

PART 6: Academic Conduct in Completing this Assessment

Academic conduct is expected to be ethical and above reproach in producing this assessment in the same way you would produce a client document as part of an accounting firm. The following table provides you with clear examples of what constitutes academic misconduct and what does not. Please carefully read this list before starting the assessment.

This integrated case study is an individual assignment. As such, no collaboration with other students is permitted in any way whatsoever. Any collaboration between students, including comparing answers, sharing ideas and research etc. constitutes academic dishonesty.

Markers will be carefully checking case studies to ascertain whether there is any indication that collusion has taken place (particularly those students that were in the same groups during the semester for the PBLs).

Students who are found to have committed academic misconduct as detailed below will be immediately referred to the QUT Business School academic misconduct committee.

Please note that penalties will be applied not only to the student(s) who have used this information but also to the student(s) who have shared this information.

To this end, each student is required to sign a student integrity declaration confirming that they have not used or plagiarised the work of others (more details are contained on page 30 of the case study).

More information on plagiarism and QUT’s range of penalties that can be imposed can be found at: https://cms.qut.edu.au/__data/assets/pdf_file/0008/638981/student-academic-misconduct-penalty-matrix.pdf

Examples of what constitutes (or does not constitute) Academic Misconduct

| Does Constitutes Academic Misconduct | Does not Constitutes Academic Misconduct |

| 1. Using a case study (or any part thereof) of another student from a previous semester. This includes obtaining a soft or hard copy of a previously used annual report from a prior semester and overtyping or re-typing any part and submitting such as part of your submission. | 1. Using a listed public company’s annual report, a listed unit trust’s annual report or a set of model financial statements as a basis of determining the format, layout and structure for the financial report of The Flavours of Italy Unit Trust. |

| 2. Using a case study (or any part thereof) of another student doing the unit this semester. This includes a student that has been in your group/team during the semester. | 1. Using the words contained in a listed public company, a listed unit trust’s annual report or a set of model financial statements (eg. the Note 1 Significant Accounting Policy note) and using these words/sentences for The Flavours of Italy Unit Trust. |

| 3. Including a requirement that may have been part of a previous semester’s case study and including it this semester. |

PART 7: Submission Instructions

Please collate the following documents into one pdf document in the following order:

- Signed Student Integrity Declaration (on page 30);

- Criteria Sheets (on pages 31 and 32);

- Part 1 – Your self-reflection (requirements detailed on page 4);

- Part 2 – Your MYOB Adjusting Journal Entries dated 30 June 2019 including your revised MYOB Profit and Loss Statement and Balance Sheet as at 30 June 2019;

- Part 3 – The 2019 Annual Report of The Flavours of Italy Unit Trust (including the external financial statements, notes to the accounts, the Trustee’s Declaration, the Accountant’s Compilation Report and Minutes of Meeting of the Trustee showing the accounting distribution of 50% to each unitholder) in that order; and

- Part 4 – The 2019 income tax return of The Flavours of Italy Unit Trust, including the one-page tax reconciliation (to be included at the end of the last page of the trust’s tax return) as well as the tax distribution minute.

QUT’s Turnitin Electronic Submission of Assignments Tool

The integrated case study should be submitted via Turnitin no later than 11:59 pm on Tuesday 9 June 2020.

Details of how to submit the case study through Turnitin are provided as follows.

Turnitin is an electronic tool for student assignment submission, originality checking and online marking. It is one of the centrally supported assignment submission services available at QUT. Students are required to submit the integrated case study through Turnitin.

There are several benefits of submitting your case study through Turnitin:

- Students do not need to be on campus to submit the assignment; and

- Students will receive an e-mail receipt for a successful assignment submission.

After you submit your assignment successfully, there is a green banner displaying ‘Paper Successfully submitted’.

Once the due date/time has passed, students are not able to resubmit the assignment (even if they realise they have submitted the wrong version or wish to change or edit the document). Hence, it is the responsibility of each student to ensure that the complete assignment (and correct version) is submitted by the due date.

Students should refer to the following website for further information and submission details.

https://www.student.qut.edu.au/studying/learning-with-technology/assessment/turnitin-page/turnitin.

- Where to go for Help?

The IT Helpdesk is the first point to contact for assistance with Turnitin, computer or system-related queries. However, please bear in mind that the IT Helpdesk closes weeknights at 10:00 pm.

- Phone: (07) 3138 4000

- Web Address: http://www.ithelpdesk.qut.edu.au/

INTEGRATED CASE STUDY

THE FLAVOURS OF ITALY UNIT TRUST

Background Information:

The date is Friday 28 June 2019. The time is 3:00 pm. As the external accountants and tax advisors of The Flavours of Italy Unit Trust, you are in a meeting with your clients, Mario Lombardi and Luciano Rossi.

The purpose of the meeting is to review the draft MYOB management accounts of The Flavours of Italy Unit Trust for the year ended 30 June 2019 which have been prepared by their part-time bookkeeper, Amanda Hawkins.

The restaurant has been closed all day as Mario, Luciano and the staff have spent all morning conducting the annual stocktake counting stock on hand.

Unfortunately, Amanda is unable to attend the end-of-year meeting but has provided you with the MYOB data file. She asks that if you make any adjustments, you do so directly into the MYOB data file and date any adjustments 30 June 2019.

Amanda has advised you that she has entered all of the trust’s transactions for the 2019 financial year (unless otherwise indicated). She has reconciled the trust’s bank account and has reconciled the GST payable and GST receivable accounts in the Balance Sheet.

Please note that the MYOB data file that has been presented to you is not a “real” client MYOB data file.

All that was done was to enter journal entries so as to arrive at closing balances at 30 June 2019. Hence, please do not analyse the journal entries already existing in this MYOB data file.

In your meeting, Mario and Luciano have made you aware of the following information:

The bookkeeper, Amanda, has not recorded any depreciation/amortisation in respect of any non-current assets acquired by the trust during the 2019 financial year. She asks you to calculate the relevant depreciation amounts and process these depreciation/amortisation journal entries for the 2019 financial year directly into MYOB (refer page 7 for details of depreciation rates for accounting purposes).

On 1 August 2018, The Flavours of Italy Unit Trust purchased the following assets outright (all amounts shown GST-exclusive):

(a) Leasehold Improvements:

- Fit-out (consisting of non-slip floor tiles, ducted air-conditioning, lighting, benches and signage) – $142,800.

(B) Property, Plant and Equipment:

- Cash register – $5,250

- Desktop computers and printer – $6,680

- Refrigerators and freezers – $62,410

- Kitchen equipment and utensils – $26,350

- Ovens – $30,780

- Crockery, glasses and cutlery – $4,240

- Tables and chairs – $16,990

(c) Computer Software:

- MYOB AccountRight and retail point of sale software – $14,140

(d) Liquor Licence:

- Liquor licence – paid to The Queensland Office of Liquor and Gaming Regulation – $8,000.

Amanda coded all of these purchases to their various asset category accounts in the Balance Sheet. No other non-current assets were purchased during the year.

Note: There are 334 days from 1 August 2018 to 30 June 2019.

Please refer to the accounting useful lives for each of the abovementioned assets on page 7 of the case study.

3). On 8 October 2018, The Flavours of Italy Unit Trust entered into a non-cancellable lease agreement to finance the acquisition of a motor vehicle (ie. a Ford Transit SWB Van) that will be used exclusively in the business. Details of the finance lease agreement are as follows:

Details of the finance lease agreement are

- Fair value of van (GST-exclusive) $42,000

- Present value of the minimum lease payments

(including the present value of the guaranteed residual). $42,000

- Amount financed under the lease agreement $42,000

- Lease term 5 years

- Number of monthly lease payments 60

- Monthly lease payments (GST-inclusive) due on the 8th day of each month $770

- The first lease payment of $770 is made in advance on 8 October 2018.

There is no interest on the first lease payment.

- Thereafter, 59 monthly lease payments are due on the 8th day of each month. The 60th and final lease payment is due on 8th September 2023.

- Under the lease agreement on 8th September 2023 (being the same date as the final $770 lease payment, the trust is also required to make the guaranteed lease residual payment of $9,000 (GST-inclusive). The trust intends to pay out the guaranteed lease residual in 5 years time and take full legal possession of the van.

- Total GST-inclusive lease payments (including the guaranteed residual) $55,200

- Total GST-exclusive lease payments (including the guaranteed residual) $50,182

- Useful/(effective) life of the van (same for accounting and taxation) 8 years

- Depreciation policy: the trust uses the straight line method for accounting purposes and the SBE simplified depreciation regime for small business entities for taxation purposes.

- The estimated residual value of the van at the end of the eighth year $Nil

Note: There are 266 days from 8 October 2018 to 30 June 2019.

Mario has provided you with the original finance lease agreement. All of the above information is contained in the lease agreement. Unfortunately, the lease agreement does not stipulate the implicit interest rate. Hence, you will need to calculate the implicit interest rate when preparing your EXCEL lease spreadsheet.

Ignore any accrued interest between 8 June to 30 June each year.

In other words, the outstanding lease liability at 30 June 2019 is effectively the amount of the outstanding lease liability at 8 June 2019.

Mario and Luciano use the car to pick up stock items such as food, meats and vegetables, as well as for delivering food as part of the home delivery option. The van is used 100% for business purposes.

The van is garaged every day and night of the year at the restaurant. As it is not available for private use by any employee, there are no fringe benefits tax implications in respect of the vehicle.

As there is no private use, all of the running costs associated with the van shown in the Profit and Loss Statement are fully tax-deductible to the trust.

In the MYOB management accounts that Amanda has provided you with, on 8 October 2018, she has correctly recorded the motor vehicle in the Balance Sheet by debiting it for its GST-exclusive cost of $42,000 and crediting the corresponding lease liability for $42,000. This amount was recorded as a non-current liability.

A total of nine (9) lease repayments of $700.00 each (GST-exclusive) have been made between 8 October 2018 and 30 June 2019. Amanda has debited the 9 lease payments for their GST-exclusive amount totaling $6,300.00 to the “lease payments” account which is shown as an expense in the Profit and Loss Statement and credited “cash at bank” for this amount.

Being a lease, the trust has claimed back the $70.00 GST input tax credits associated with each lease payment on the 8th day of each month in the trust’s Business Activity Statement (BAS) for the relevant quarters. Amanda has correctly debited the total GST paid of $630.00 associated with the 9 monthly lease payments to the “GST receivable” account in the Balance Sheet.

Amanda did not know how to split the monthly lease payments of $770 between interest expense and reduction of the lease liability and asks that you prepare a lease schedule showing this split and, most importantly, put through the appropriate journal entry recording the split between these two amounts to 30 June 2019.

There is no need to include the lease schedule itself in your submission to this case study.

4). On 31 July 2018, Flavours of Italy held an opening party at the restaurant for local store owners, suppliers and selected residents and their families. The primary purpose of the evening was to allow these invited guests to sample the food and drinks on offer and allow them to interact not only with each other but with Mario and Luciano and to experience not only the great food on the menu but also the wonderful service.

A total of 40 guests attended the opening party. No employees attended the opening party. You can assume that at this point, that Mario and Luciano were not yet formally employed by the trust. Hence, they were not yet employees for FBT purposes. The occasion was purely social. The cost of the opening party came to $2,200 (GST-inclusive). Amanda coded the entire $2,200 to “opening party” in the Profit and Loss Statement. Ignore any GST consequences.

5). The Christmas party was held on Friday 21 December 2018 at a nearby licensed seafood restaurant. Mario and Luciano and the four other employees attended the Christmas party. No customers were invited. The cost of the Christmas party came to $378. This amount was coded to “Entertainment – Christmas Party” in the Profit and Loss Statement. Ignore any GST consequences.

6). Apart from Items 4 and 5 above, the trust did not provide any other meal entertainment to clients or employees whatsoever during the 2019 financial year.

7). For FBT purposes, the trust adopts the actual method in valuing its meal entertainment fringe benefits. No FBT applies as in the case of the opening party, due to the fact that no meal entertainment was provided to employees. In the case of the Christmas party, whilst the meal entertainment was provided to employees, the cost per head per employee was under $300. Hence, no FBT applies. The amounts of these expenses shown in the Profit and Loss Statement are shown GST-inclusive as the trust is not entitled to claim back any GST input tax credits associated with these expenditure items.

8). Mario, Luciano and the staff undertook a stocktake on the morning of 30 June 2019. Closing stock (which consists of food, food ingredients and drink – both alcoholic and non-alcoholic) has been reliably ascertained at $22,040 (GST-exclusive).

The trust adopts a periodic inventory system and uses the weighted average cost inventory valuation method for both accounting and taxation purposes. The opening balance of inventory on the first day of business (ie. 1 August 2018) was $16,088.

The bookkeeper, Amanda, did not know how to input the closing stock figure of $22,040 into the MYOB management accounts and specifically asks you to process the relevant journal entry/entries directly into MYOB on her behalf. She has left the opening stock figure of $16,088 (which she entered on 1 August 2018) in the MYOB management accounts as she did not know how to do the adjustment.

9). The employees of The Flavours of Italy Unit Trust are as follows:

- Mario Lombardi (General Manager of the restaurant);

- Luciano Rossi (Head Chef);

- an assistant chef;

- a waiter;

- a waitress; and

- a delivery driver.

The total salaries and wages for these six employees are shown in the Profit and Loss Statement. There are no outstanding (accrued) wages owing to any of the employees at 30 June 2019.

10). Each full-time employee is entitled to four (4) weeks paid annual leave per annum. Part-time staff are entitled to pro-rata annual leave. At 30 June 2019, Amanda had not yet recorded a journal entry to accrue the annual leave for these employees. Based on the projected salaries of when each employee is expected to take their annual leave, the total provision for annual leave (in respect of all employees) as at end of financial year totals $12,420. The trust policy is that all annual leave must be taken within 12 months. No annual leave was taken by any employee during the 2019 financial year.

No sick leave was taken by employees during the 2019 financial year. No provision for sick leave should be made in the 2019 accounts as no employee is considered likely to take more than their allocated sick leave entitlements. The sick leave is non-accumulating and non-vesting meaning that no entitlement (and therefore, no accrued sick leave) is carried over to the following financial year for any employee.

Similarly, no employee is eligible for long service leave. As such, no provision for long service leave should be made in the 2019 accounts as, at 30 June 2019, it is not currently considered probable that any employee will reach the 10-year employment target with the trust in order to qualify for long service leave.

11). Due to surplus cash in the bank account, on 1 June 2019, The Flavours of Italy Unit Trust prepaid three months rent (for the months of June, July and August 2019) totalling $13,200 (GST-inclusive) to their landlord.

By making this payment to the landlord, this means that the store’s rent is prepaid until 1 September 2019. Amanda recorded the following journal entry in MYOB on 1 June 2019:

| DATE | PARTICULARS | POST REF | DEBIT | CREDIT |

| 1 June | Rent expense | 6-1190 | 12,000 | |

| GST receivable | 2-1040 | 1,200 | ||

| Cash at bank | 1-1010 | 13,200 | ||

| (Payment of three months rent of $4,400 per month GST-inclusive) |

Ignore any GST consequences. If any adjusting entries are required, please record this entry in the general journal in MYOB.

Note: If an adjustment is required for the prepaid rent, instead of apportioning for the number of days, simply apportion for the number of months.

12). On 19 November 2018, The Flavours of Italy Unit Trust purchased 1,000 shares in BHP Billiton Limited at a cost of $32.80 per share (including brokerage). Amanda recorded the shares in the trust’s Balance Sheet at their cost of $32,800. These shares were purchased with the view to holding them for the long-term. Hence, why they were recorded as a non-current asset.

No other shares were bought or sold during the 2019 financial year. As at 30 June 2019, the share price of BHP Billiton Ltd was trading on the ASX at $29.80 per share (fair value of $29,800).

As previously mentioned, the trust has made an irrevocable election to present subsequent changes in fair value of these shares through Other Comprehensive Income (OCI) instead of recording increases and decreases in fair value through profit or loss.

13). On 22 March 2019, The Flavours of Italy Unit Trust received a fully franked dividend from BHP Billiton Ltd of $630. Amanda (the bookkeeper) has recorded this dividend received in the MYOB Profit and Loss Statement as revenue. The relevant company tax rate was 30%.

14). The initial set-up costs of $1,640 incurred to establish the trust and associated accounting and legal fees are shown as an expense in the Profit and Loss Statement under “Establishment Costs”. Assume that these costs were incurred directly by the trust on 1 August 2018.

15). As outlined in the business plan, The Flavours of Italy Unit Trust signed a three-year non-cancellable operating lease to rent commercial premises at 144 Lancaster Avenue in Hendra for $4,000 per month (GST-exclusive commencing 1 August 2018).

A 2.5% annual increase is to take effect on 1 August each year. There is an option in the lease agreement to renew the lease for an additional three years at the expiration of the current lease and in perpetuity thereafter.

At this stage, Mario and Luciano see no reason why the lease would not be renewed when the current lease term expires.

Application of Accounting Guidance Note No. 2007/4

Assume that the trust does not apply Accounting Guidance Note No. 2007/4 Accounting for Operating Lease Expenses and hence, does not wish to “straight line” the trust’s operating lease commitments in relation to the rent over the three-year period.

16). Mario and Luciano were delighted that there was surplus cash in the trust’s bank account even after prepaying the rent (refer Note 11). On 2 June 2019, they invested $25,000 into a 60-day term deposit with Bank of Brisbane at an interest rate of 2.50% per annum.

Interest totalling $102.74 will be paid by the bank on maturity 60 days later (ie. 31 July 2019). The trust does not intend to rollover the term deposit once it matures. Amanda recorded the $25,000 in the “term deposit” as a current asset in the Balance Sheet of the trust.

Note: There are 29 days from 2 June 2019 to 30 June 2019.

Additional Event that Occurred After 30 June 2019:

Assume that it is now Friday 26 July 2019. You are in the process of preparing the financial statements of The Flavours of Italy Unit Trust for the year ended 30 June 2019. The 2019 financial statements are yet to be signed off by Mario and Luciano.

You have just received a telephone call from Mario advising that they have just received notification of a pending legal suit from a customer who suffered extreme and violent food poisoning a day or two after having dinner at their restaurant on Saturday 13 July 2019.

Luciano and Mario are rigorously denying the claim and have engaged solicitors to defend the claim on their behalf. They claim that the customer’s food poisoning had nothing to do with the food that was eaten at their restaurant. The solicitors for Luciano and Mario agree and consider that the likelihood of the restaurant losing the case is around 25 percent.

Whilst it is too early to assess the likelihood of losing the lawsuit, the person is suing the trust for $60,000 for out-of-pocket medical expenses, loss of earnings from not being able to work for four weeks as well as the emotional trauma suffered as a result of the food poisoning.

No journal entries have been recorded by Amanda in the MYOB management accounts in relation to this transaction as Amanda did not know what to do.

Additional Facts:

- The MYOB management accounts have been prepared on an accruals basis.

- The trust is on the accruals basis for income tax purposes.

- The Flavours of Italy Unit Trust is registered for the GST. It’s ABN is: 38 101 211 321.

- The trust adopts the cash attribution basis for the GST and lodges its Business Activity Statements (BAS) on a quarterly basis.

- The unit trust’s accounts were not required to be audited for the 2019 financial year (and were not).

- The trust funds (ie. corpus) comprise 200,000 x $1.00 units totalling $200,000. Each family trust contributed $100,000 when the trust was settled.

- The two unitholders (each owning 50% of the issued units) are The Lombardi Family Trust (Mario is the trustee of this discretionary trust) and The Rossi Family Trust (Luciano is the trustee of this discretionary trust).

- As the unit trust does not pay tax, any profit is distributed 50% to each unitholder. Even if the profit is not distributed in cash at year-end, the profit distribution is credited to each unitholder’s respective loan account. Each unitholder subsequently includes their share of profit in their respective family trust’s financial statements and income tax return.

- The trustee of The Flavours of Italy Unit Trust is Flavours of Italy Pty Ltd. The ABN for the corporate trustee is: 19 341 841 014.

- Mario and Luciano are the two directors of the corporate trustee.

- The share capital of Flavours of Italy Pty Ltd (the corporate trustee) is $2. Mario and Luciano each hold 50% of the issued share capital of the company (ie. $1 fully paid ordinary share).

- As previously mentioned, the corporate trustee does not trade nor holds any other assets (other than $2 cash on hand) and has no liabilities in its own name whatsoever.

- All PAYG withholding tax owing in respect of employee’s salaries and wages have been remitted by The Flavours of Italy Unit Trust to the ATO by the due dates. The 30 June 2019 PAYG withholding tax has not yet been remitted to the ATO. This amount of $14,776 shown in the Balance Sheet as a current liability will be paid to the ATO when the trust lodges its June 2019 Business Activity Statement with the ATO (sometime before the due date of 28 July 2019).

- The three quarterly Business Activity Statements (BAS) for the September 2018, December 2018 and March 2019 quarters have been lodged with the ATO by their due dates and the net GST owing (ie. GST payable minus GST receivable) for each quarter have been paid to the ATO.

- The amount of GST payable ($26,150) and GST receivable ($11,040) shown in the Balance Sheet at 30 June 2019 (giving a net GST owing to the ATO of $15,110) represents the amount GST collected and paid by the trust to the ATO in respect of the June 2019 quarter. This net amount will be paid to the ATO before the due date for lodgement of the BAS (ie. before 28 July 2019).

- As a trust does not pay any income tax in its own name, no PAYG instalments have been paid by The Flavours of Italy Unit Trust to the ATO and none are owing in respect of any quarterly BAS lodged.

- The $250,000 loan from the Bank of Brisbane that the trust took out is unsecured. This loan is fixed at a fixed interest rate of 6.0% per annum and fully repayable in five years time. There were no initial borrowing costs associated with this bank loan. The borrowings are unsecured and no assets were pledged as security against these borrowings.

- The trust has been making loan repayments and as at 30 June 2019, the outstanding balance of the loan is $210,480 (split in the MYOB Balance Sheet as $62,550 current and $147,930 non-current). The bookkeeper, Amanda, has correctly split each loan payment between interest paid and reduction of the loan liability.

- The trust has been making the compulsory 9.5% employer-sponsored superannuation contributions into each employee’s superannuation fund on a quarterly basis on the last day of each quarter based on each employee’s ordinary times earnings (OTE). Accordingly, all superannuation amounts owing in respect of the 2019 financial year have been paid into each employee’s superannuation fund by 30 June 2019 (including the amount owing in respect of the June 2019 quarter).

- According to the MYOB management accounts prepared by Amanda, the trust derived an accounting profit. However, Amanda did not know how to allocate this profit between the two unitholders and hence, MYOB has automatically transferred the net profit from the profit and loss statement to “retained profits” in the Balance Sheet.

- The amounts contained in the MYOB data file are based on the actual results of The Flavours of Italy Unit Trust for the period 1 August 2018 to 30 June 2019 (ie. 11 months of trading). These actual figures override any amounts contained in the business plan and in any of the PBLs during the semester relating to The Flavours of Italy Unit Trust. Students should also note that the figures contained in the initial business plan were only budgeted amounts, not actual amounts.

- Background information relating to The Flavours of Italy Unit Trust and personal details involving Mario and Luciano can be found in the business plan.

- Furthermore, ignore any additional information in PBLs during the semester relating to Flavours of Italy (eg. PBL 1 Part B when students were asked to develop the chart of accounts). Only use information contained in the case study provided to you.

- Impairment testing has been conducted at 30 June 2019 in respect of all assets (including the leased motor vehicle). There is no indication that any asset shown in the Balance Sheet is impaired.

- In the MYOB management accounts, no non-current asset has been revalued (or devalued) to fair value. All assets are shown at their historical cost.

- The legal expenses ($3,193) and repairs and maintenance ($2,022) shown in the Profit and Loss Statement are all tax-deductible.

- The staff amenities ($944) shown in the Profit and Loss Statement relates to tea, coffee and biscuits purchased by the trust and provided to employees for consumption on the business premises during morning and afternoon tea breaks.

- The sundry expenses ($1,712) shown in the Profit and Loss Statement represent non-tax deductible expenses.

- The uniforms ($960) have been approved as non-compulsory uniforms by AusIndustry and have been entered on the Register of Approved Occupational Clothing.

- Workers compensation ($632) relates to the workers compensation premium paid to Workcover Queensland on behalf of the employees and is tax-deductible.

- The motor vehicle expenses ($5,750) represent the running costs associated with the motor vehicle (including petrol and oil, registration, insurance and RACQ). Depreciation has not been calculated or included as part of this figure.

- Insurance of $7,793 represents premiums paid by the trust during the 2019 financial year to Maximus Insurance in respect of both public liability insurance and trustee’s and officer’s professional indemnity insurance.

- Any adjusting journal entries made in MYOB (through the “Record Journal Entry” function) should be made without adjusting for the effects of the GST (except where otherwise indicated in the case study). Please date all of your MYOB adjusting journal entries as 30 June 2019.

- In other words, all journal entries you decide to make to the MYOB data file provided should be made using the GST tax code “N-T” (except where otherwise indicated in the case study).

- In terms of depreciation for accounting purposes, please refer to the table on page 7 of this case study which outlines each depreciable asset for accounting purposes, its estimated useful life and depreciation rate. Assume that all assets listed have an estimated residual value of $Nil.

- As noted on page 7, for accounting purposes, the trust will use the straight-line depreciation method for all depreciable assets (including the leased motor vehicle).

- As previously noted, in the case of accounting depreciation/amortisation journal entries, students are requested to combine depreciation/amortisation amounts for each individual asset class and show depreciation per asset class (ie. leasehold improvements, property, plant and equipment, computer software, the liquor licence and the leased motor vehicle).

- This should result in five (5) separate depreciation journal entries in MYOB. Do not put through separate MYOB journal entries for each of the eleven individual assets listed on pages 19 and 20 of the case study.

- In terms of depreciation for taxation purposes, being a small business entity (SBE), the trust will depreciate those eligible depreciating assets using the simplified depreciation regime (refer rules below).

- Streamlined depreciation rules apply to small business entity taxpayers who elect to take advantage of these optional depreciation concessions.

- A summary of these tax depreciation rules that apply in respect of depreciating assets acquired after 12 May 2015 and before 29 January 2019 are summarised below.

(i) an immediate 100% deduction applies in respect of depreciating assets costing less than $20,000 (GST-exclusive); and

(ii) depreciating assets costing $20,000 or more (GST-exclusive) are automatically pooled (ie. lumped together) and are depreciated in a general small business pool at the diminishing value rate of 30% per year (15% DV in the first year).

- For taxation law purposes, computer software is considered to be a depreciating asset. Hence, the MYOB accounting software and retail point of sale software costing $14,140 are subject to the same SBE simplified depreciation rules outlined in the paragraph above.

- Due to the above, the trust is using different depreciation rules for accounting and taxation purposes.

- The trust is also keen to take advantage of any other SBE tax concessions that it may be eligible for.

- In the case of the fit-out, as this constitutes capital works for income tax purposes, please use the rates contained in Division 43 of the ITAA (1997).

- For taxation purposes, the liquor licence is to be depreciated over two (2) years using the prime cost depreciation method. In other words, it is the same calculation as for accounting purposes.

- As there are no income tax consequences in the financial statements of the trust, there are no temporary differences. Hence, there are no DTA’s and/or DTL’s recorded in the financial statements of a trust.

- All calculations should be made on a daily basis. The ATO has a useful facility where you are able to calculate the number of days, being:

https://www.ato.gov.au/Calculators-and-tools/Host/?anchor=CalculateDays&anchor=CalculateDays#CalculateDays/questions.

AYB 339 ACCOUNTANCY CAPSTONE

STUDENT INTEGRITY DECLARATION

(MUST BE COMPLETED, SIGNED AND SUBMITTED BY EACH STUDENT

AND INCLUDED AS THE FIRST PAGE OF YOUR SUBMISSION

When submitting your assessment to Turnitin, you will be declaring the following:

- I have complied with all the unit coordinator’s instructions for this assessment.

- I understand that plagiarism involves using another person (or persons’) ideas or work as one’s own, as explained in the QUT Manual of Policies and Procedures at C5.3 which is available at: http://www.mopp.qut.edu.au/C/C_05_03.jsp.

- I understand that it is a breach of academic integrity to assist, or allow another person/s to copy our work.

- I declare that this work is entirely my own, and no part of it has been copied from any other person’s (or persons’) words or ideas, except as specifically acknowledged through the use of inverted commas and appropriate referencing.

- I declare that no part of this assessment has been written for me by any other person or persons except where such collaboration has been authorised by the unit co-ordinator concerned.

- I give permission for our assessment to be reproduced (copied), communicated, compared with other sources and stored (including electronically) in order to detect plagiarism and agree that plagiarism detection software may be used.

- I declare that this assessment has not been submitted, in whole or in part, for any other unit at QUT or any other institution, unless authorised by the relevant unit co-ordinator.

I, the undersigned, declare that I have read, accepted and agree to the statements in the Declaration above, which are true and correct.

Student Number

Student Name

Signature

Note: If this declaration is not completed, signed and submitted, your case study will not be marked.

Reference ID: #getanswers2001191